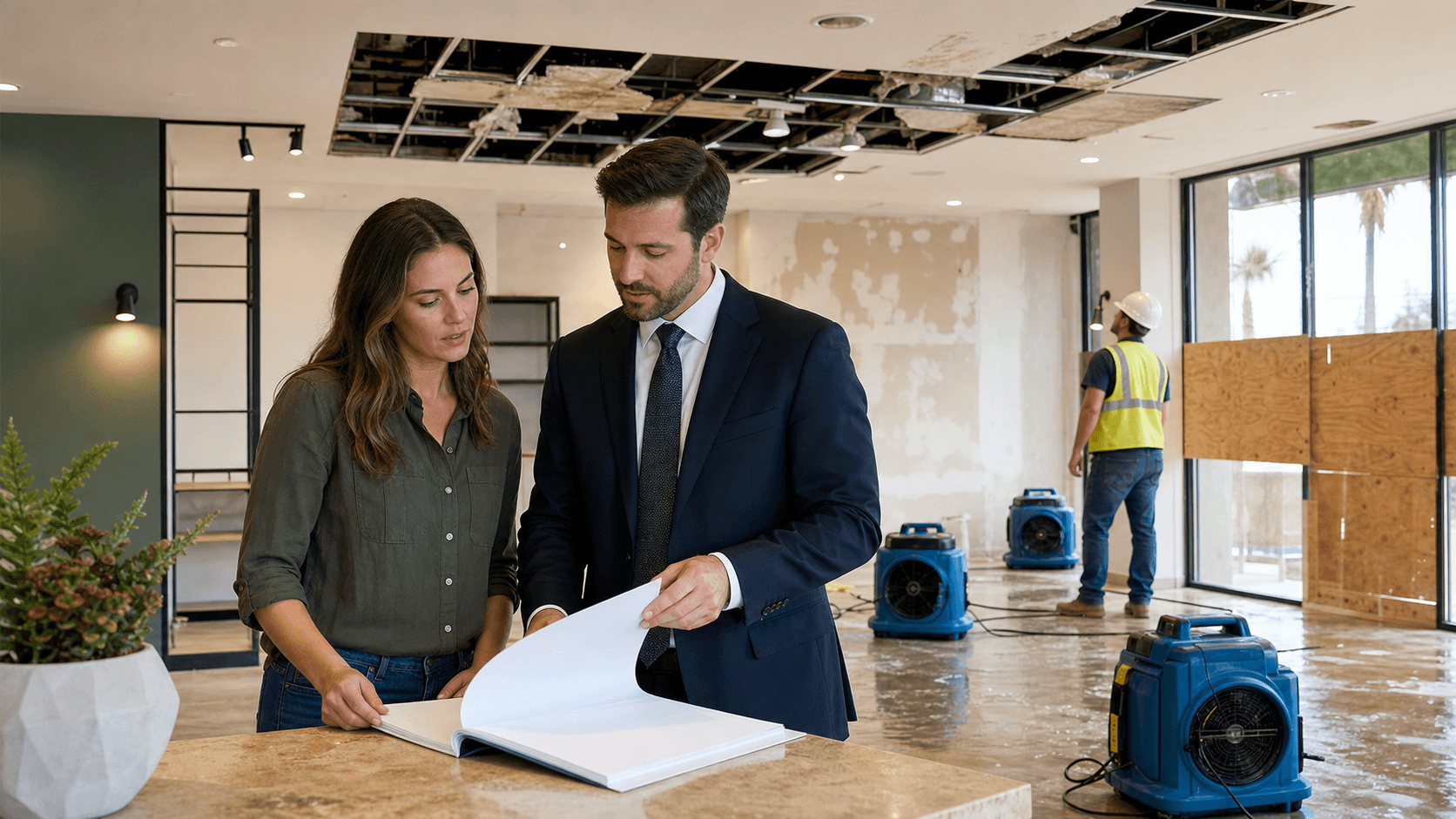

A single large property loss can shock the entire cash flow of a Texas commercial building. When hail, windstorm, hurricane, tornado, fire, smoke, or internal water damage hits, the question is not just who fixes what. The hard questions are who still owes rent, whose insurance is paying, and how long the business can stay alive while repairs drag on.

Those answers do not turn on general ideas of fairness. They turn on the exact wording of the lease and how that wording fits, or does not fit, with the property policy and business interruption coverage. At Lundquist Law Firm, we see what happens when those documents are not aligned. We are a Texas-based firm that represents policyholders only in significant commercial property and business interruption disputes. We do not draft leases, but we regularly litigate the fallout when a serious loss collides with an imperfect lease and a slow or underpaying insurer.

Aligning Lease Structure with Real-World Property Losses

Texas commercial landlords and tenants often assume that a "big loss" means rent stops for a while and insurance picks up the tab. That is not automatic. Rent abatement, who repairs, and who can walk away often depend on:

- The casualty and damage provisions in the lease

- The building and business interruption policies in place

- How the insurers handle scope, pricing, and timing

Sophisticated owners and tenants treat the lease as part of the insurance plan. That means deciding in advance:

- Who insures the building shell and who insures build-out and contents

- Whether rent abates, and if so, how it is calculated and for how long

- What happens if repairs take longer than the policy's business income period

When those issues are not thought through, the gaps usually appear for the first time right after a hurricane roof loss, a tornado hit to a distribution center, or an internal water loss that shuts down a key tenant.

How Texas Commercial Leases Interact with Property Policies

Most Texas commercial leases follow a basic split of risk. The landlord usually handles the structure and core systems. The tenant often handles interior improvements, trade fixtures, inventory, and its own business interruption coverage. The "damage and destruction" or "casualty" section is where the real allocation lives.

Lease terms like "substantial damage," "partial loss," "total loss," and "constructive loss" are not just filler. They are often tied to:

- Whether rent is fully or partially abated

- Whether the landlord must restore, and to what standard

- Whether either party can terminate early

On the insurance side, the building policy and any endorsements should be read along with those lease terms. Key points usually include:

- Building limits and whether they match replacement cost

- Ordinance or law coverage for code upgrades that can delay or change repairs

- Extra expense, civil authority, and ingress or egress coverage that impact how long operations are restricted

We regularly see leases that quietly assume "insurance will cover it" while the actual commercial property or business income forms have waiting periods, tight sublimits, exclusions, or narrow period-of-restoration language. That mismatch puts both rent and revenue at risk when a claim becomes contested.

Structuring Rent Abatement, Termination, and Coverage

Rent after a casualty is rarely one simple number. A typical Texas commercial tenant may pay:

- Base rent

- Additional rent such as CAM, taxes, and insurance pass-throughs

- Percentage rent based on sales or other metrics

Each part can be treated differently if the space is partially or fully unusable. Common approaches include:

- Automatic rent abatement based on the percentage of square footage or operations lost

- Abatement that tracks when the landlord's "loss of rents" or "rental value" coverage actually responds

- No rent abatement unless the space is totally unusable, which may leave a tenant paying for space it cannot reasonably operate in after serious damage

The lease should say who decides when space is "untenantable" or "unsuitable for its intended use." Insurers often try to downplay the level or length of damage to limit business interruption or rental value payments. That can pull landlord and tenant into conflict if the lease is vague.

Termination rights also matter. Many parties negotiate rights to exit the lease if:

- Restoration is not substantially complete by a certain date

- The loss occurs near the end of the lease term

- Code upgrades or ordinance requirements make repair uneconomic

Those decisions are often tied to live coverage disputes about scope, pricing, and how long repairs should reasonably take, issues that sit at the center of what a Texas commercial property damage lawyer handles.

Business Interruption, Rental Value, and Realistic Timelines

Business interruption coverage is its own language. Terms like "business income," "extra expense," "period of restoration," and waiting periods do not always match what a lease or a business owner expects. Landlords usually rely on rental value or loss of rents coverage. Tenants often carry their own business income coverage.

Many leases are quiet on key points:

- Which party must carry which coverage types

- Required limits and minimum indemnity periods, such as 12, 18, or 24 months

- Whether coverage must match the rent abatement and casualty structure in the lease

After large Texas events like major windstorms, hail events, or significant fires, three problems show up again and again:

- Restoration takes longer than the policy's business income period

- Soft costs, code upgrades, and inspection delays stretch the schedule

- Insurers dispute scope or causation, pushing for cheaper "patch and paint" repairs and shorter downtime

Owners and tenants do better when they match lease terms to realistic restoration timelines for that building type and market. That includes not accepting a generic certificate of insurance as proof that the coverage actually tracks what the lease needs for rent abatement and business interruption support.

Handling Claims, Disputes, and Strategic Steps Before and After a Loss

After a significant loss, the process usually starts fast and then slows down. There is emergency mitigation, initial inspections, and early estimates. Then the insurer issues reservation of rights letters, trims the scope, and pays in phases. During all of this, rent obligations and business survival are on the line.

We often see:

- Scopes that miss hidden or complex damage

- Estimates that push cosmetic or short-term repairs instead of full restoration

- Causation arguments like "pre-existing wear and tear," "cosmetic hail," or "old leaks" to cut the covered damage

Those tactics cut building payments, which then impact rent abatement, tenant viability, and the landlord's cash flow. A Texas commercial property damage lawyer focused on policyholders can help align the claim strategy with the lease realities by:

- Reviewing the lease's damage, rent, and termination provisions alongside the policies

- Pressing the carrier for a complete scope and accurate valuation, including code and soft costs where covered

- Addressing business interruption or rental value calculations tied to real restoration timelines

Before a loss, owners and tenants can reduce risk by:

- Reviewing casualty and damage clauses with both coverage and claim disputes in mind

- Clarifying which party must carry which policies and for how long a loss of income period

- Aligning rent abatement and termination rights with realistic recovery paths for that specific asset

After a loss, careful early steps help preserve leverage:

- Read the lease's damage and rent sections right away

- Document the condition of the building and how operations are disrupted

- Coordinate between landlord and tenant so the reported "story of the loss" is consistent

- Avoid signing broad releases or accepting low payments that do not restore both the property and the income stream

At Lundquist Law Firm, we work with Texas commercial policyholders, including owners, landlords, and tenants, when large property and income losses are tied up in coverage disputes, claim delays, and underpayments. Aligning lease rights, rent expectations, and insurance outcomes is not just a legal exercise; it is a way to protect the long-term value of both the property and the businesses that operate there when a serious property loss hits.

Protect Your Commercial Property Investment Today

If your business is facing significant property damage, you do not have to navigate the insurance process on your own. At Lundquist Law Firm, our Texas commercial property damage lawyer can evaluate your situation and help you pursue the coverage you are owed. We are ready to review your policy, assess your losses, and explain your legal options in clear terms. To discuss your next steps, please contact us today.